You walk into an open house.

And instantly know.

This is the one.

You start picturing your furniture in the living room. Your mornings in the kitchen. Maybe even mentally claiming your side of the garage already.

Your agent asks:

“Awesome. Are you pre-approved?”

You confidently say yes.

But what you actually have… is a pre-qualification.

And that difference?

It can absolutely cost you the house.

I see this happen all the time with buyers who are just starting the process.

They think they’re ready to make offers…

But they haven’t actually gone through a real mortgage pre-approval yet.

And in a competitive market, sellers and listing agents know the difference immediately.

Let’s break it down in plain English.

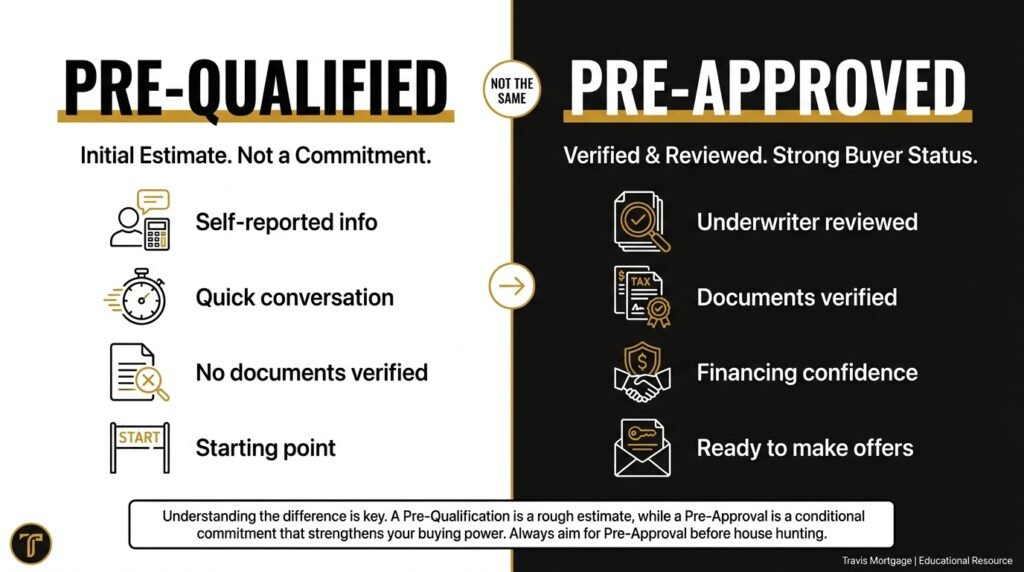

Pre-Qualified: What It Actually Means

A pre-qualification is basically the “starting conversation.”

It’s quick.

Usually takes 10–15 minutes.

You tell a lender things like:

- Your estimated income

- Your monthly debts

- Your credit score range

- Your estimated savings

The lender may run a soft credit check and say something like:

“Yeah, based on what you told us, things look pretty good.”

And that’s fine.

Pre-qualification has a purpose.

It gives you a rough idea of where you stand.

But here’s the important part:

👉 Nothing has actually been verified yet.

No underwriter has reviewed documents.

No income has been confirmed.

No bank statements reviewed.

No employment verified.

In other words:

It’s not a commitment to lend.

And sellers know that.

That’s why a pre-qualification letter doesn’t carry much weight in a competitive situation.

It’s a starting point.

Not a finish line.

Pre-Approved: What It Actually Means

A mortgage pre-approval is completely different.

This is where things get real.

Instead of just talking about your finances…

You actually document them.

That means submitting things like:

- Pay stubs

- W-2s or tax returns

- Bank statements

- Employment information

- ID and supporting documents

Then an underwriter reviews everything.

And this is the key difference most buyers don’t understand:

👉 An underwriter is the person who ultimately decides whether the loan gets approved.

Not the loan officer.

Not the online calculator.

The underwriter.

So when your file has already been reviewed upfront, you’re in a much stronger position.

What Does “Conditional Approval” Mean?

You’ll sometimes hear the term:

Conditional approval

That sounds scary to buyers… but honestly, it’s normal.

It just means:

“Everything looks good, assuming the remaining conditions are met.”

Those conditions are usually tied to the specific property:

- Appraisal

- Title work

- Insurance

- Final employment verification

In other words:

The hardest part is already done.

That’s a huge advantage.

How Long Does a Pre-Approval Take?

Typically, a fully underwritten mortgage pre-approval can take anywhere from a few days to about a week depending on complexity.

And once completed, it’s generally valid for a set period of time before documents need updating.

The important part isn’t the exact timeline.

It’s that you’ve already done the heavy lifting before finding the house.

Why This Matters in a Competitive Market

Here’s the reality:

Listing agents can tell the difference between a pre-qual and a real pre-approval almost immediately.

And sellers care about one thing more than anything else:

👉 Confidence the deal will actually close.

Because financed deals fall apart more often than people realize.

Income changes.

Debt ratios shift.

Documents don’t match.

Underwriting catches issues late.

That’s why sellers lean toward buyers who feel more certain.

A fully underwritten pre-approval sends a completely different message.

It says:

“This buyer is serious. Their financing has already been vetted.”

And in multiple-offer situations…

That matters.

A lot.

Want to Go Even Further?

For buyers who want the strongest possible position, this is also where programs like Cash to Win come into play.

That takes things a step beyond even a traditional pre-approval by helping qualified buyers compete with cash-level strength.

But regardless of whether you use a strategy like that…

A real pre-approval is the foundation.

The Team Goltz Advantage

This is one of the biggest things we focus on with buyers at Team Goltz.

We don’t want you walking into open houses with a “maybe.”

We want you walking in prepared.

That means offering fully underwritten pre-approvals, not just quick pre-quals.

So when the right house shows up:

- You know your numbers

- You know what you can comfortably afford

- Your offer carries more weight

- You can move fast without scrambling

And honestly?

It just makes the entire process less stressful.

Because you already handled the hardest part upfront.

Final Thoughts

If you’re serious about buying a home…

Don’t start the process with a pre-qualification and assume you’re ready.

Get the real work done first.

A true mortgage pre-approval gives you clarity, confidence, and a much stronger position when it’s time to make an offer.

And in this market, that difference matters.

If you want to get fully pre-approved, or just understand where you stand, let’s talk.

📞 763-360-4507

We’ll walk through your situation and build a plan that actually puts you in a position to win.