John and Henry both got promoted.

Same company.

Same role.

Same jump in income.

They both went from making about $185K a year to roughly $285K.

From the outside?

Both looked successful.

But what happened next completely changed their financial future.

John upgraded everything immediately.

New truck.

$850/month payment.

Moved into a nicer apartment.

$2,200/month rent.

Started eating out more. Traveling more. Financing more.

Eighteen months later, John decided he wanted to buy a house.

And despite making great money…

He barely qualified.

Higher debt.

Higher monthly obligations.

Worse rate than expected.

Meanwhile, Henry didn’t change much.

Same lifestyle.

Same apartment.

No flashy upgrades.

Instead:

- Paid off debt

- Saved aggressively

- Lowered credit card balances

- Built reserves

When Henry walked in 18 months later?

No debt.

Strong credit.

Real down payment.

He got exactly the house he wanted…

And still had about $20K sitting in the bank afterward.

Same income increase.

Completely different outcome.

And honestly?

I see versions of this every single week.

How Debt-to-Income Ratio Actually Works

This is the part most buyers never really get explained properly.

When lenders look at mortgage approval, one of the biggest factors is your:

Debt-to-Income Ratio (DTI)

That’s just a fancy way of saying:

👉 How much of your monthly income is already committed to debt payments.

Every lender has limits on how much debt they’re comfortable approving compared to your income.

And here’s the important part:

A car payment doesn’t just “hurt a little.”

It directly impacts how much house you can qualify for.

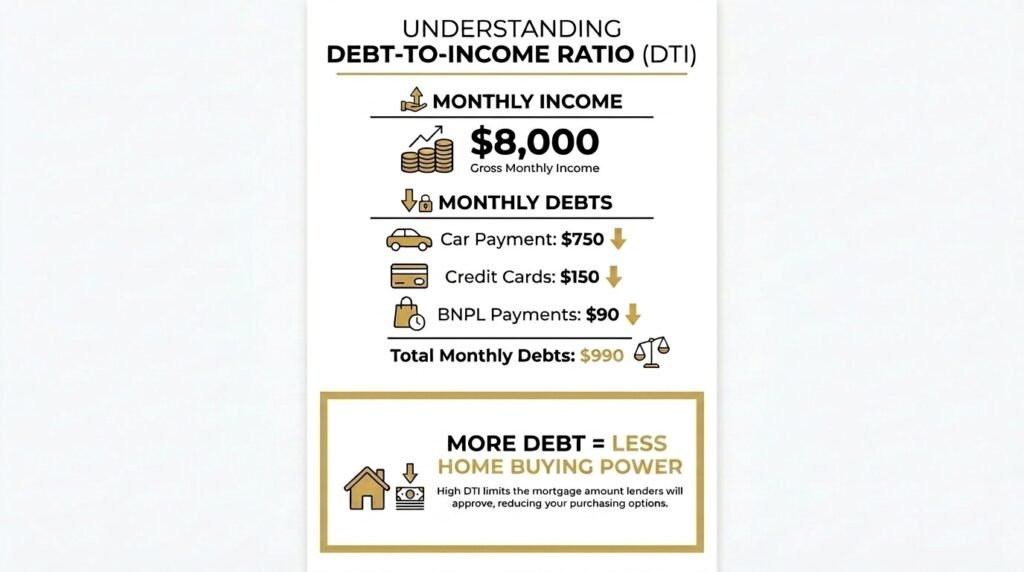

For example:

Let’s say you have:

- $8,000/month gross income

- Minimal debt

- Strong credit

You might qualify comfortably for a certain payment range.

Now add:

- $750 truck payment

- $150/month credit card minimum

- $90/month BNPL payments

Suddenly your qualifying power drops fast.

Because lenders don’t look at what’s “left over.”

They look at fixed monthly obligations.

That’s why someone making great money can still struggle to qualify.

Income matters.

But monthly debt matters just as much.

Sometimes more.

The Car Payment Problem Nobody Talks About

This is probably the biggest thing hurting buyers right now.

And most people don’t even connect it to their mortgage.

A lot of buyers are carrying:

- $600

- $700

- Even $800+ monthly car payments

And with today’s interest rates?

Some of those loans are sitting at 18–19%.

That’s brutal.

You’re hemorrhaging money every month…

While simultaneously crushing your mortgage qualification.

And here’s where it gets worse:

A lot of people are upside down on those vehicles.

Meaning they owe more than the car is worth.

So now they’re stuck.

The payment hurts their DTI.

The negative equity traps them in the loan.

And qualifying becomes harder every month.

This is why I tell people all the time:

👉 Sometimes the fastest way to qualify for the home you want isn’t saving more money.

👉 It’s getting rid of the thing that’s draining it.

That one decision alone can completely change someone’s buying timeline.

Credit Cards: The Hidden Lever Most Buyers Ignore

Credit cards affect mortgage approval in two major ways.

The first is:

Credit Utilization

This is the percentage of your available credit you’re using.

And yes, it matters more than most people realize.

A good rule of thumb:

- Under 30% utilization = decent

- Under 18% = even better

This is one of the fastest ways to improve a credit score before applying for a mortgage.

And higher scores can mean:

- Better rates

- Better loan options

- Lower monthly payments

But here’s the second issue that’s becoming a huge headache lately:

Buy Now, Pay Later Apps

Klarna.

Afterpay.

Zip.

Affirm.

A lot of buyers think:

“It’s only small payments.”

But underwriting sees something different.

Multiple repayment obligations.

Auto-drafts.

Documentation issues.

Cash flow inconsistencies.

And honestly?

These apps create documentation nightmares sometimes.

Especially when buyers have several running at once.

If you’re serious about buying in the next 6–12 months…

Start winding those down now.

Your future mortgage process will be dramatically cleaner.

What to Do 6–12 Months Before Buying a Home

This is where planning changes everything.

Most mortgage problems don’t happen because people are irresponsible.

They happen because nobody explained the strategy early enough.

Here’s what I’d focus on before buying:

1. Know Your DTI Before House Hunting

Run the numbers early.

Don’t wait until after you fall in love with a house.

A quick conversation now can save months of frustration later.

2. Don’t Finance Anything New

This is a big one.

No new:

- Cars

- Furniture

- Toys

- “0% financing” purchases

Every new payment chips away at buying power.

3. Pay Credit Cards Down Below 30%

Ideally below 18%.

This can move scores surprisingly fast.

And small score improvements can create meaningful mortgage differences.

4. Get Rid of BNPL Apps

Seriously.

The fewer moving pieces in underwriting, the better.

Clean financials win.

5. Talk to a Lender Early

Not two weeks before you want to make an offer.

Early planning gives you options.

And most issues are fixable with enough lead time.

Here’s the truth most people miss:

👉 Most buyers don’t need more income to buy the right home.

👉 They need a better plan before they start looking.

Final Thoughts

These are patterns I see every single week.

And almost all of them are fixable.

Not overnight.

But absolutely fixable with the right strategy and enough time.

The buyers who win long term usually aren’t the ones making the most money.

They’re the ones making intentional moves before they start house hunting.

If you want help building a plan, let’s talk.

📞 763-360-4507

👉 https://booking.travisgoltz.com/widget/bookings/goltz-booking

The conversation is free. And it may save you a lot of frustration later.