The average first-time home buyer is now 40 years old.

That’s the highest it’s ever been.

And a big reason for that?

Most people think you need:

- 20% down

- Perfect credit

- Years of saving

So they wait.

And wait.

And wait some more.

But here’s the reality:

Minnesota has multiple first-time home buyer programs designed to close that gap.

The problem?

Most buyers don’t hear about them until it’s too late… or not at all.

Let’s walk through what’s actually available in 2026 — and how this could apply to you.

The 20% Down Payment Myth (Let’s Clear This Up First)

Let’s get this out of the way.

You do not need 20% down to buy a home.

That’s one of the biggest misconceptions I see.

Here’s what’s actually common:

- FHA loans: as little as 3.5% down

- Conventional loans: as low as 3% for first-time buyers

- VA loans: 0% down for eligible veterans and active military

- USDA loans: 0% down in eligible rural and suburban areas

So if you’ve been sitting on the sidelines thinking you need a massive savings account…

You might be closer than you think.

Now let’s talk about the programs specifically designed to help even more.

MHFA Programs (Minnesota Housing Finance Agency)

When people search for Minnesota first time home buyer programs 2026, this is usually what they’re looking for.

The Minnesota Housing Finance Agency (MHFA) offers some of the most widely used programs in the state.

Here are the key ones to know:

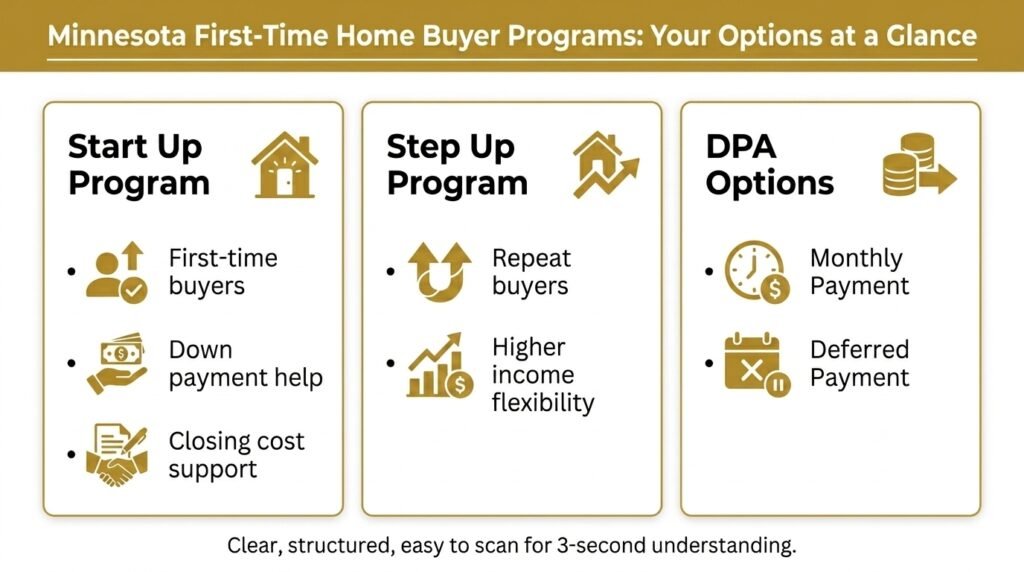

Start Up Program

This is designed specifically for first-time home buyers.

It provides:

- Down payment assistance

- Help with closing costs

- Competitive loan options

This is where a lot of buyers get their foot in the door.

Step Up Program

This one is for:

- Repeat buyers

- Higher-income households

If you don’t qualify for Start Up, this is often the next place to look.

Down Payment Assistance Options (Important)

This is where things get interesting.

There are typically two main types:

1. Monthly Payment Assistance

- Comes with a small monthly payment

- Lower upfront burden

2. Deferred Payment Assistance

- No monthly payment

- Paid back later (often when you sell or refinance)

Which one makes sense depends on your situation.

Homebuyer Education Requirement

Most MHFA programs require a homebuyer education course.

And honestly?

That’s a good thing.

It helps you understand the process, avoid mistakes, and feel more confident going into one of the biggest purchases of your life.

Important Note

Income limits and assistance amounts vary by county and are updated regularly.

That’s why it’s important to talk through your specific situation instead of guessing.

Other First-Time Buyer Programs in Minnesota (2026)

MHFA is a big piece of the puzzle.

But it’s not the only one.

There are other options that can make a big difference depending on your situation.

Local and Lender-Specific Programs

There are programs available through lenders (including ones we use at Granite Bank) that you won’t find at big national banks.

These can include:

- Additional down payment assistance

- Flexible qualification options

- Stacking opportunities with other programs

These are often overlooked — but they can be a game changer.

👉 Learn more here:

https://travisgoltz.com/down-payment

USDA Loans (0% Down Options)

A lot of people assume USDA only applies to farmland.

Not true.

There are plenty of suburban areas in Minnesota that qualify.

Key benefits:

- 0% down

- Competitive rates

- Flexible income limits

This is one of the most underused programs out there.

VA Loans (For Veterans and Active Military)

If you’re eligible, this is one of the strongest loan options available.

- 0% down

- No private mortgage insurance (in most cases)

- Competitive terms

If this applies to you, it’s absolutely worth exploring.

FHA Loans (Flexible Entry Point)

FHA is often the go-to for first-time buyers.

- 3.5% down

- Lower credit score requirements

- Widely accepted

It’s not perfect for every situation, but it opens the door for a lot of buyers.

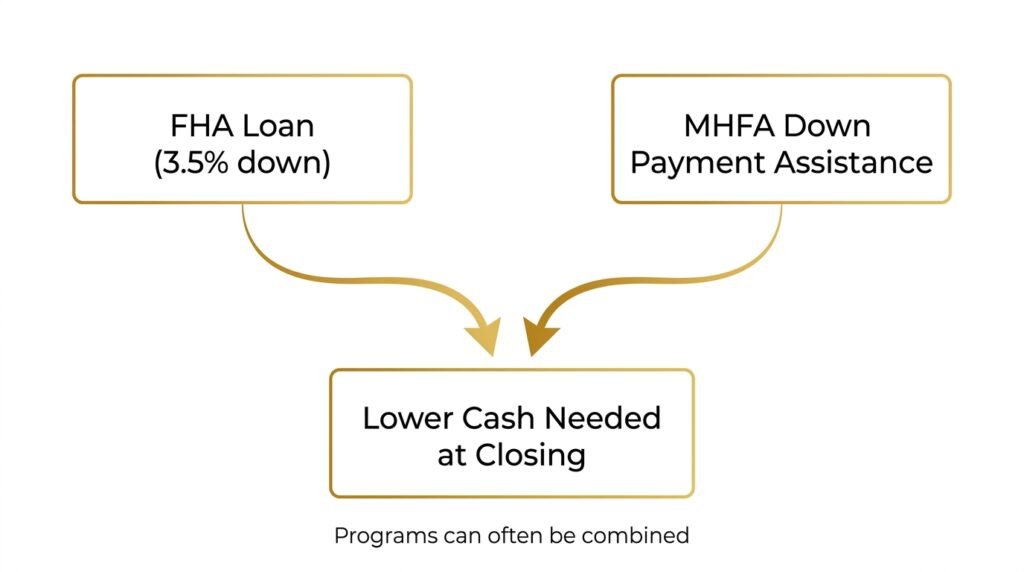

How to Combine Programs (This Is Where Strategy Matters)

Here’s something most articles won’t tell you:

You can often combine programs.

For example:

- FHA loan

- PLUS MHFA down payment assistance

That combination can significantly reduce your upfront costs.

This is where working with someone local really matters.

Big banks tend to plug you into one product.

We look at the full picture and build the right combination.

Because the goal isn’t just to get approved.

👉 It’s to put you in the best position possible.

What Should You Do Next?

If you’re thinking about buying in the next 6–12 months, here’s where I’d start:

1. Check your credit score

Know where you stand. No guessing.

2. Don’t wait until you’re “ready”

Talk to a lender early — even if you’re months out.

3. Explore your options

Don’t assume you don’t qualify.

A lot of buyers disqualify themselves before ever having a real conversation.

Final Thoughts

Homeownership in Minnesota is more accessible than most people realize.

The programs exist.

The options are there.

The real question is:

Do you have the right strategy… and the right person helping you put it together?

If you want to see what you might qualify for:

👉 https://travisgoltz.com/down-payment

Or just book a quick call:

We’ll walk through your situation and map out your next step.

No pressure. Just clarity.